STAFDA 2014 Session Preview: Abe WalkingBear Sanchez

The Cost of Missed Opportunities — Eliminate the hidden obstacles to repeat sales and profitability.

|

|

|

WHEN AND WHERE:

STAFDA cash flow consultant Abe WalkingBear Sanchez will reveal how to identify and eliminate the costs of missed sales and credit opportunities from 9:00 -11:00 a.m. on Sunday, Nov. 9, 2014.

|

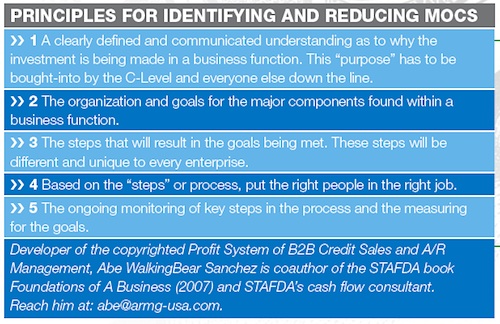

Missed Opportunity Costs (MOCs), profit that would have resulted from doing something that wasn’t done, are difficult if not impossible to account for, but that doesn’t make them any less real. Because my focus is on B2B or commercial credit sales and A/R management, I’ll be addressing credit- and A/R-related MOCs, but the same principles apply across all business functions.

The P&L statement accounts for how revenue (money in), also called the “top line,” is transformed to the “bottom line,” which will be either a profit or a loss.

Between revenue, which results in most cases from the sale of products or services, and the “bottom line” lie expenses. These expenses will vary from business to business, but can be lumped together as “fixed costs” that don’t change with production or sales levels, and “variable costs” which vary depending on production and sales. When and whether or not you get paid on credit sales are “variable costs.”

It is important to understand that 95 percent or more of all B2B/commercial sales involve payment at a later date. The short-term money due from customers is often one of the largest assets a business has and, as a rule, it is also the greatest source of working capital.

The credit and A/R function plays a role in both the approval of new and repeat sales and in making sure that the cash resulting from these transactions keeps flowing into a business. The credit and A/R function also has a role to play in customer service and customer retention levels and in ongoing constant improvements throughout the entire supply/production chain.

Even though MOCs aren’t listed on the P&L, they can have a huge “bottom line” impact. Once understood and identified, MOCs can contribute to both increased revenue and a reduction of both fixed and variable costs. Anything that’s a hindrance or obstacle to closing a first sale — or to keeping existing customers paying and making additional purchases — represents a MOC.

Perceptions Hurt Profitability

There’s an old and out-of-date understanding that credit is an accounting function whose performance is measured not by the “profit” it helps generate, but by the “risk” involved. Credit has been called the sales avoidance department, the place where sales go to die and, as one CEO put it, the “ugly stepchild of accounting.” This “risk at the expense of profit” thinking leads to MOCs that easily exceed the expense of slow- and no-pay customers.

Most companies use risk-based performance measurements of DSO and bad debt rather than profit-based measurements. In so doing, they create substantial MOCs. The variable costs of time, value of money and bad debt too often mal-define and limit the profit role that is played by the credit and A/R function. Once credit and A/R related MOCs are understood, identified and action is taken to avoid them, profitability is enhanced and the “bottom line” goes up.

But as the great Yogi Berra once said, “There are some people who, if they don’t already know, you can’t tell ‘em.”

New Understanding

When the total costs of finding and selling to new business customers are taken into consideration, most first commercial sales are a wash — there is little or no profit. Additional sales to existing business customers are the most profitable, with each additional sale being more profitable than the last.

How credit sales approval and A/R are understood and managed will directly impact both first and additional sales.

Credit and A/R management’s primary purpose is sales support. It is not an accounting function. Those involved with credit sales approval need to know that their job is to find a way to make profitable sales happen and that performance will be measured by the percentage of applied-for dollars approved. If marketing and sales have done their jobs, the credit function should be able to approve more than 100 percent of applied-for dollars. And yes, of course the risk factor must be taken into consideration, but it should not be the focus.

Those involved in PDCM (past due customer management) need to understand that their role is ensuring “the completion of the sale.” It is not “collections,” the enforcement of payment. They need to know that the job is to identify why a customer hasn’t paid and resolve the issues involved. If they do this, the company will be in position to get the most profitable sales, repeat sales. Again, each additional repeat sale is more profitable than the last.

Measure performance based on customers retained and repeat sales made. That way, you will be measuring for where you want to be instead of where you’ve been. Stop using negative words like “debtor” to refer to those who put the food on your table and to whom everyone in your company is beholden. Customers, even when they are past due, are the reason everyone shows up for work. Start thinking in terms of expanding credit lines and not “credit limits.”

In the process of working with sales, customers and almost everyone else in the supply/production chain, the credit and A/R people will come across “areas of opportunity for improvement.” Tell them that they need to let everyone know about these new efficiencies that will drive down your costs and your customers’ costs of doing business.

Use credit to increase new and repeat sales, raise customer service and customer retention levels, identify and control the very small percentage of past due customers who are a genuine risk of failing to pay and drive down the costs of inefficiencies. Do this and the profits that would have resulted from doing something that wasn’t done will show up on your bottom line.

Allow Thinking

Whether it’s in the credit department or any other part of an organization, employees are often encouraged to “toe the line” and follow existing ways of doing things. Their actions are often dictated by what others are doing, which is where limiting jargon like “industry standards” and “best practice” come from. This doesn’t encourage new ways of thinking — quite the opposite. And that’s where MOCs really set in.

Like it or not, the impetus for change usually has to come from the top and when it does, it cascades throughout an organization. The result can be good or disastrous, but when it’s good, it’s very good.

If employees at all levels are encouraged to do what they know is right, even — no, especially — if it brings into question traditional thinking, then you can identify and limit, if not say goodbye to, MOCs.

Credit is “the selling of a product/service based on payment at a later date” — the key word being “selling.” The ONLY reason for any business to make the investment or to create the costs that go with extending credit terms is to get profitable sales that would otherwise be lost. CS

STAFDA cash flow consultant Abe WalkingBear Sanchez will show attendees how to recognize and root out old paradigms and establish a new understanding of — and models for — creating more profitable credit sales. Reach him at www.armg-usa.com.

CONTRACTOR SUPPLY MAGAZINE

The June/July 2024 issue of Contractor Supply magazine is here!

This digital edition is sponsored by BECK AMERICA Inc.

Our cover story, Success Plan, visits MC Tool and Safety Sales in Blaine, Minnesota. This family business is transitioning from father to daughter leadership in one of the Twin Cities' top communities.

Also in this issue are our industry updates on: Nailers and Staplers; Fastening Systems; Air Compressors and Accessories and a special contribution from STAFDA Online Marketing Consultant Bob DeStefano on Digital Marketing Game Changers.

This digital edition is fully searchable and contains live links to every advertiser and new product listing. Click away!