STAFDA Cash Flow Consultant: When Salespeople Become Bread Men

This article began in the February/March 2012 issue of Contractor Supply and concludes in the April/May edition. It is presented here in its entirety.

|

|

Part 1: How to measure and combat sales force complacency

Bread men are delivery guys who pick up a truckload of fresh bread and drive from store to store, filling shelves. If there is an empty slot, they fill it. All they need to care about is that the right bread goes in the right slot. When salespeople start thinking like bread men, a business is in big trouble.

I was working with a large regional distributor whose market share was shrinking. The sole-source provider of a high-end home construction product in an area of the country where the population doubled and then doubled again during the 30 years that the manufacturer held the patent on this product; this company had seen both it’s sales and profitability grow for three decades.

Then the patent expired and the product began to be manufactured in China. Although this company still maintained the largest share of the market, competitors had undercut their price by 30 percent or more and their sales had dropped off.

During a session with the company’s VPs, looking for ways to turn things around, the sales VP said something that left me dumb-struck. “I know we are losing market share, but we still make good money, so I’m not worried,” he said.

I was in the Navy and any time your ship is taking on water, it’s not a good sign. Just because your head is still above the waterline doesn’t mean there’s nothing to worry about — just the opposite, you should be manning the pumps and fixing the leak while you are still above water.

At that point I turned to the credit manager, who was there with the finance VP, and asked him how many new customer credit applications or new customer information forms he processed each month. He wasn’t real sure because he didn’t track them but he guessed about 10 a month. I then asked the sales VP how many salespeople he had in their six-state area. To his credit, he knew — it was 26.

I then said something to the effect that 10 new potential credit customers a month by 26 salespeople meant that on average each sales-person was bringing in a potential new customer every 90 days or so. “No”, said the CM, “only five or six of the salespeople ever turn in a new customer request for credit.”

A good profit-focused credit manager, just like the sales manager, should know and should be reporting on how many new customer requests for a credit line are being submitted by sales and processed by credit. He needs to know and report on who is bringing in the new business, what type of business/market segment these new customers fall into, the amount of credit applied for vs. the amount of credit approved and of course he needs to report on how long it took to process these new pending sales. And if a potential customer is not approved, everyone needs to know why not.

Thirty years of profitable growth without having to compete is not a good thing, especially when things change. The salespeople in this company had become “bread men,” — they had long ago forgotten how to sell. The credit manager in this company had time to kill so he was running two home-based retail businesses on the side. Of course, much of what he was doing with the side businesses was on his employer’s time and dime.

This company was not a team effort — it was every man/woman for him/herself.

Vital signs

CEOs, business owners and managers need to monitor their company’s B2B credit sales and A/R vital signs. In medicine, basic vital signs include temperature, pulse rate, blood pressure and pain level. They are measurements taken to assess critical body functions and as such are an essential part of the communication between doctors, pharmacists, nurses, therapists and others regarding a patient’s state of being. And so it is with vital signs for critical business functions like credit, sales and A/R (accounts receivable) management and a company’s state of health.

The management team of a business must establish clearly understood goals for the different business functions in their organization and then be able to establish means by which to monitor the progress or lack of progress being made toward those goals.

They need to employ the right people capable of carrying out the tasks and then give them the needed training. Management must have reliable information/reports by which to monitor the execution of plans and to measure performance against the established goals.

Lastly, but most important, the management team must constantly work to ensure that everyone understands the goals and that everyone is working together toward the goals.

Before the vital signs for the credit sales and A/R management area of business can be establish, explained, monitored and measured CEOs, business owners and senior managers must know and understand what the best possible outcome for this business function looks like — and yet many companies misunderstand and underutilize the credit sales and A/R management function. Here are some basics:

- 90 percent or more of all B2B sales involve payment at a later date — credit terms are extended

- A/R — short-term money due from the sale of products or services based on payment at a later date — is often one of the largest assets many companies have. On average the A/R is 40 percent or more of the total assets (less with manufacturers, more with service companies and some distribution companies).

- Next to cash on hand, the A/R is among the most the most liquid of assets, being but one step removed from money in the bank. A/R is very often the greatest source of working capital.

- In the course of approving credit sales and then managing the resulting A/R, the credit sales and A/R team interfaces with customers, sales, marketing, accounting, operations, the warehouse, service, vendors/suppliers, attorneys, transportation and many others in the supply/production chain. These areas contain a wealth of valuable information and knowledge that often is not shared or utilized to its fullest profit potential.

What’s the best outcome and the vital signs for credit sales and A/R management?

Credit Sales

When all the costs involved with a new sale are considered, often the investment made in getting a new customer to the point where they want to buy exceeds the profit to be earned in the first sales. Profit comes from long-term customers and repeat sales.

One vital sign is the number of new customer information forms (better than preprinted, one-size-fits-all credit applications) that are being submitted by sales to credit.

If the number of submitted new customer information forms is down during key times of the month compared to last month and/or last year, salespeople can be incentivized to turn the month around. This can be done by daily contests that include the credit area’s timely processing of the submitted new customer

information forms.

Another vital sign during key times of the month is the total amount of credit that has been applied for vs. the percentage of that applied-for credit that has been approved by the credit area. A good profit-directed credit manager can be worth three to four good salespeople if they view pending sales as their highest priority and focus on finding ways to approve profitable sales while remaining confident of payment.

A profit-focused credit manager will look for ways to turn a $10,000 credit customer into a $100,000 customer via creative terms and conditions of sale. When salespeople focus on quality customers and credit people focus on both finding a way to make the deal happen and on granting a larger credit line (never credit limit) than was requested; the percentage of credit approved should be more than 100 percent of the applied-for credit amount.

If during key times of the month the percentage of applied for credit-approved drops, is it

because the quality of the customers is down, the economy is bad or is the sales force calling on the wrong market? Or is it because the credit guy isn’t working hard enough to find ways to make profitable sales happen?

Part 2: Using PDI to monitor monthly sales performance

What is watched gets done

Sometimes management sends confusing messages to the credit manager. It will stress the need to get pending and profitable sales on the books and then measure the credit area’s performance based on DSO and percent of bad debt. This leads the credit area to focus on risk rather than on sales and profit.

Sometimes management itself doesn’t understand or know the proper profit approach to credit approval, and therefore can’t provide the credit area with the understanding and training on how to weigh the customers’ profile and their past performance with the

company’s own product value at time of sale . . . so as to maximize sales and minimize risks.

A/R Management (not collections)

The proper management of A/R (accounts receivable) results in good cash flow, sustained repeat sales and controlled bad debt.

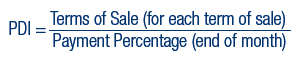

The vital sign that is directly connected to cash flow, repeat sales and bad debt is the PDI (payment days index) at the end of the month and the daily payment percentage during key times of the month.

Start with the beginning total A\R balance as of the first of the month. This means all A/Rs regardless of age. Any new credit sales made during the month will be picked up in the next month’s beginning total A/R balance.

For example, let’s say that our total A/R balance as of the 1st of the month is $1,000. Track payments and credits on those invoices that make up the beginning total A/R balance. During key times of the month (the 10th and the 20th) we want to compute the Payment Percentage as of that date by dividing the amount paid/credited by the beginning total A/R balance.

If, by the 10th we have been paid/credited $200 of the beginning $1,000 total balance, our payment percentage as of the 10th is 20%. We can compare this month’s 10th day payment percentage against last month’s 10th day payment percentage.

If last month’s 10th day payment percentage was 40% and this month it’s 20%, it doesn’t necessarily mean that we are doing a poorer job this month than last. If there’s a variation of the payment percentage, it’s not a matter of good or bad, but of why? That’s the question to ask.

A lower payment percentage may be due to as simple a reason as the credit and A/R person going on vacation and no one following up on past due A/R. It may also be a

matter of a product/service with a lower product value being sold to someone with less that perfect past performance (pay record). Or it could be due to the accounts being worked in alphabetical order rather than by largest dollar first.

If by the 20th, we’ve been paid $400 of our beginning balance of $1,000 our payment percentage as of the 20th is 40%. By tracking the payment percentage during the month we can determine if we need to exert greater efforts. If we are not happy with the payment percentage as of the 20th, we have 10 days in which to turn things around.

At the end of the month, compute the PDI by dividing the payment percentage into the terms of sale. For example: at the end of the month, we have been paid $500 of our beginning A/R total of $1,000, our payment percentage is 50%, or 0.5. If we are selling on 30-day terms, our PDI would be 60 days.

If you have varying terms of sale, you must compute the PDI for each and then average them out, just as you would do with DSO.

If you have a good payment percentage, your cash flow will also be good and your established credit customers will buy more from you. As a rule, repeat sales are the most profitable, with each repeat being more profitable than the last. Keep them paying and keep them buying.

Also, a good payment percentage will contribute to controlled bad debt loss because it’s a positive indicator that the accounts are being worked and that a potential bad debt is

being identified earlier in the process when the amount of potential loss is less/lower.

What’s a good PDI?

All vital signs will vary based on the variables involved. For example, if a company’s sales and the related business activity is down, the unused capacity to do business (fixed expenses) goes up and the seller’s product value at time of sale goes down. When a low product value at time of sale is factored into the credit approval process, riskier credit sales should be approved even if this results in slower payments, a lower payment percentage and even to an increase in bad debt. If done correctly, the utilization of the unused capacity (fixed expenses) will more than off-set the slow payments and increased bad debt.

The same thinking on product value at time of sale applies to “demand” and “margin.” High product value means taking less risk, low product value means taking higher risks.

The purpose of vital signs is to draw the focus of management. Again, the question to be asked when it comes to vital signs is, “Why?”

What — Me Worry?

I’m not a mechanical sort, but I’ve learned the hard and expensive way that when the oil or service engine “idiot light” comes on it means that you’re an idiot if you don’t pay

attention to it.

In the course of approving credit sales (90 percent or more of all sales) and then managing the resulting A/R, the credit area interfaces with many of the different facets of the supply/production chain and can identify areas of opportunity for improvement.

Dr. Demming said that the true cost of errors is unknown and unknowable. Dr. Coase said that of all the frictions (cost) involved with business the greatest friction of all is the friction of failure —something going wrong somewhere. A vital sign that should be monitored and given full management attention and energy is the number of “systems problems” (somethings that went wrong somewhere) and the dollars therein involved.

Systems problems are friction, and drive up everyone’s cost of doing business — seller and buyer alike — and lead to a competitive disadvantage for all.

Smart guys pay the tuition for their education but once. Not-so-smart guys buy new engines.

The CEO was driving me to the airport at the end of the day and asked me what I thought needed to be done. I told him I’d have my written report and suggestions out to him in three days, but he again asked, “What do you think?”

Taking a chance that he might make me walk the rest of the way, I said to him, “The company needs a new bus driver; you’re the wrong guy for the job.” He took me the rest of the way, but man, it got real quiet. I sent in my report but didn’t hear back. Later I learned that the manufacturer had dropped them as a distributor and that the investors had sold the company for parts. CS

Abe WalkingBear Sanchez is the developer of the copyrighted Profit System of B2B Credit Management: a proven philosophy and set of methodologies that move the credit function from being a cost center to a profit-driven area of business. President of A/R Management Group,Inc. (www.armg-usa.com), Abe WalkingBear Sanchez is also a founding member of the international Profit Centered Credit Group.

CONTRACTOR SUPPLY MAGAZINE

The June/July 2026 issue of Contractor Supply magazine is here!

In our cover story, Service Over Scale, Idaho Tool in Nampa, Idaho follows a philosphy of immediacy, expertise, and advocacy through 40 years of change and success.

Also in this issue are Industry Updates.

This digital edition, sponsored by BECK AMERICA Inc., is fully searchable and contains live links to every advertiser and new product listing. Click away!

| Read the Articles Read the Digital Edition |