STAFDA Cash Flow Consultant: Trade Credit

A 21st Century Profit Source

|

|

In “Lean” thinking there is a line of thought that believes that: 1) All work occurring in an enterprise is interconnected; 2) Variation exists in all processes, and; 3) Understanding and reducing variation are keys to success/efficiency. I agree with #1 but as to #2 and #3, I would add some points of clarification.

To #2, I would add that variation is an ongoing given and thus new conditions and existing circumstances must drive new processes.

To #3, I’d add; understanding that every enterprise is different and unique is to understand that there is more than one path to the mountain top/efficiency, and it is the identification and elimination of contradicting beliefs, via new goals, that best contributes to new processes and new efficiencies.

A recent email from the CEO of a large regional distribution company reminded me of an article I wrote in 2001. First, here is that email, then the article, then my reply to the email and finally some thoughts about A 21st Century Profit Source . . . too often still waiting to happen.

THE EMAIL

“I am the CEO of a Fluid Power Distributors Association (FPDA) distributor. We do our due diligence up front on credit checks and over the past five years our A/R days averaged 42.

“Where there is sizable sales opportunity, our sales/inside sales employees are expected to start the qualification process before they quote a customer so they don’t waste time with someone who doesn’t/can’t pay their bills.

“We have very little write-off in a normal year and have been caught off guard by few significant bankruptcy filings over the years.

“Where we run into problems is with new or newer companies with little history or references. Ninety percent of our business is with small to medium size OEMs. Small start-up companies often offer us the most opportunity to move our products and expertise in the design and spec stages of building a new machine. These same new and newer companies carry greater risk.

“In your presentations you have stated that, on improving A/R you can be too restrictive with your credit policy and ultimately cost yourself business. We know this to be true — we recently lost approximately $150,000 worth of business at 30% GM (gross margin) for 2011 and $300,000 for 2012 because of our credit terms.

“Based on our credit check, our CFO required 1/3 down, 1/3 at delivery and 1/3 Net 30 Days due to a lack of credit history. On the initial order for $26,000, our competitor matched our pricing and took the business on Net 30 Day terms. I have a very unhappy salesman.

“Can you offer any thoughts or means for evaluating credit risk or alternatives we might have offered this customer when they balked at our terms? Are we missing any tools we could be using to help us achieve profitable growth with these small and new companies?”

Sure I can. Now, here is my article from 2001 addressing this issue.

THE ARTICLE: The Most Profitable Sale Waiting To Happen

It may seem like a contradiction, but there are times when more bad debt can mean an improvement to the bottom line.

The CEO of a $30M-a-year STAFDA house called me with this question. “Last year we wrote off $5,000 to bad debt. Do you think we’re too tight on credit approval?”

“First, let me ask you a couple of questions,” I said. “Do you have any unused capacity? Could you take on more business without having to hire any new people or take on any additional fixed expenses?”

The CEO answered “yes,” to both questions. Next I asked, “Are you currently turning down any credit sales? Are you rejecting riskier credit customers based on your terms?”

Again, the answer was “yes.” They had a long-established “risk” model based on TIB (time in business) and a customer’s payment history that they used in their credit qualification process. Based on this standard, they would judge new customers and decide whether or not to grant credit terms.

This pass/fail, black/white mindset about credit approval feeds on the use of DSO (days sales outstanding) and bad debt performance measurements and fails to factor-in the seller’s product value at the time of the sale.

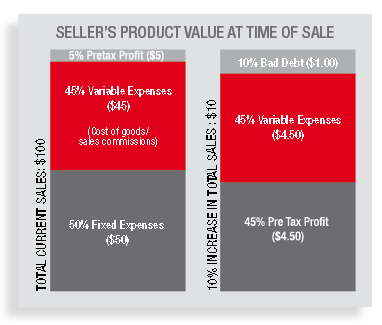

I then asked the CEO to draw a bar graph representing his total current sales, and — to keep things simple — to make the amount $100. Starting from the bottom, the first 5% or $5 was the pretax profit, the next 45% or $45 was variable expenses, such as cost of goods and sales commission.

The remaining 50% or $50 was the fixed expenses that do not fluctuate with changes in production activity level or sales such as rent, insurance, dues, equipment, loans, depreciation, fixed salaries and advertising.

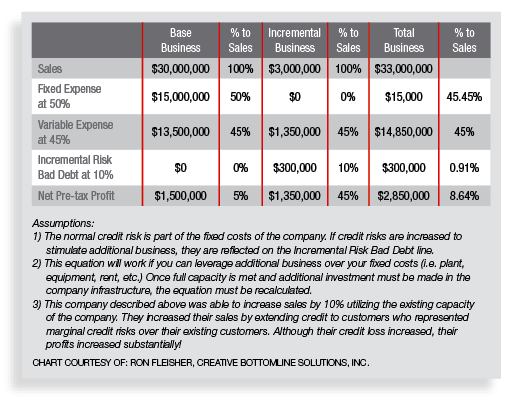

Next, I asked him to draw another bar graph representing a 10% increase in sales via new and perhaps “riskier” customers who did not fit the company’s established risk model. Of these new sales, we would budget a whopping 10% for situations where the customers would fail to pay (bad debt loss).

Of the new sales, $1 would be lost and there would still be 45% or $4.50 in variable expenses but because of the existing unused capacity to take on more business, there would be no additional fixed expenses. The pretax profit on the riskier credit sales would then leap from 5% to 45%, a 900% improvement because of the effect of “seller’s product value at the time of sale.”

When approving credit sales to new customers, most companies do a pretty good job of weighing a customer’s profile; time in business, etc. They do a fair job of checking past credit history, but all too often they fail to take into consideration their product value at the time of the sale, which will vary based on the conditions and existing circumstances at that time.

Examples:

1. A distributor of ski hat pins and sunglasses was writing off 20% of all credit sales. The only requirement for credit terms was that the customer provide a name and street address for shipping —that was it. Any new customers with a post office address were rejected out of hand.

Most companies couldn’t survive for long with such high bad debt write offs, but this company was only paying 3 cents for a hat pin and selling them for $1, a markup of 3,333% and they had a minimum sale policy. You can still go to jail for selling most products with this kind of markup, depending on the product.

Their product value at the time of the sale was very, very low compared to the selling price. Just the opposite is true of products/services with a high cost and low markup, they have a high product value at the time of the sale; for example, a banker’s product — cash.

2. A trucking company had a truck going from Denver to Omaha; on the return leg it was coming back empty. What is the “product value” of a truck coming back empty from Omaha to Denver?

Keep in mind that there’s a reason why Denver is called The Mile High City and Omaha is not — it’s uphill from Omaha to Denver. The “product value?” Zero? It is less than zero! The “product value” is a negative, a minus — minus the driver’s pay, gas, insurance and maintenance.

Knowing this, the trucking company contacted a customer with a slow payment history who had been placed on credit hold by other trucking companies. By getting 25% down and extending 60-day terms on the balance, a load was found for the return leg. And if this customer failed to pay the balance? Is all bad debt bad? NO, It depends on the product value at the time of the sale.

Slow turning Inventory has a low “product value,” as do products with a short shelf life such as cut flowers. Before the airlines reduced the number of flights and aircraft in service, flights commonly had a percentage of empty, unsold seats that, once the door of the craft closed, had a negative product value. That’s why two people sitting next to each other could pay very different fares. Today, new conditions and existing circumstances have changed the product value and what we pay to fly.

Businesses with customers standing outside their door with money in hand and wanting to buy, have high demand and have a high “product value.” The same companies with little or no new traffic have low demand and low “product value.”

Fail to take into consideration “product value” at the time of sale and you may well be passing up some of your most profitable sales.

And what about the CEO doing $30M a year? I ran into him at the next STAFDA annual meeting and we grabbed lunch. His credit sales and A/R were up, as were his turntime on the A/R and bad debt losses (but nowhere close to 10%). His biggest obstacle in factoring in “product value” was his credit manager, who had always been told, “All bad debt is bad.”

Trade Credit: Part 2

The following is the conclusion of Abe's article. This section ran in the June/July edition of Contractor Supply magazine.

In part one of this article, I relayed the story of a CEO whose biggest obstacle in factoring in “product value” was his credit manager, who had always been told, “All bad debt is bad.”

Here in part is my reply to him.

Before money was invented, each party in a transaction had to need or want what the other party had to trade. Business transactions were severely limited by the “barter system.” Money created a medium of exchange with an established value that was accepted in return for goods and services and business transactions expanded.

Credit on a person-to-person basis probably existed even before money, but modern trade credit, or commercial/B2B credit, really came into full being in the 20th Century. With it came an expanded movement of products and services.

However, use of B2B credit for most of the 20th Century was mainly local and the emphasis was on the “risk factor” in selling product or service based on payment at a later date. Twentieth Century credit was about risk and loss avoidance, which was justified by the conditions that existed for most of the century, such as limited communication and information technology, the legal system and the lack of much competition.

During this time credit was rightly thought of a “privilege,” as a favor to select customers, and the performance of the credit function was correctly measured by DSO (days’ sales outstanding) and by the percent of credit sales that failed to pay altogether. All bad debt was bad.

This “risk avoidance” mentality was reinforced in the 1950s following World War II when the United States was the only major industrial society left unscathed by the war. Not only had American production capacity been left untouched by the war, it had in fact greatly expanded and had been focused on producing goods for the war, not for consumers.

After the war, many Americans who worked to support the war had savings in banks or “war bonds.” They also had babies, millions of them. Today, between 8,000 and 10,000 Americans turn 65 every day. The “baby boom” created a growing demand for goods/services. Many American women who had left homemaker roles to work in munitions plants and factories during the war never returned to the “hearth.” More earners meant more demand.

The devastated industries and cities of Europe and Japan had to be rebuilt too. This also fed global demand and because America had escaped wholesale devastation, we had little in the way of competition.

So, these were the conditions in the third quarter of the 20th Century (1950 to 1975):

- Pent up and growing demand

- Shortages

- Limited competition

And then things, as they have a way of doing, changed.

New Paradigm, Old Thinking

Once their industrial capacity was rebuilt with new and more efficient infrastructure, European, Asian and other economies sprang to life. In the last quarter of the 20th Century production caught up with demand, and then surpassed it. Quality in products, processes and services became the new norm. Competition became worldwide; big box stores and cyber stores competed with the old traditional outlets for goods/services. The world changed except for how most companies managed credit.

In 2008 the world entered the first global economic downturn since 1946. During this and afterward, many commercial lenders restricted lending: Banks cut back on business credit, including lines of credit on business credit cards.

In 2010 the world economy started to rebound. China (+10.1%), Taiwan (+8.3%), India (+8.3%), Brazil (+7.5%), and South Korea (+6.1%) recorded the biggest GDP gains. China also became the world’s largest exporter and its GDP surpassed that of Japan, making it the second largest economy in the world.

Continuing uncertainties in the mortgage and financial markets, combined with a glut of goods/services and an aging population, resulted in slower growth in Japan (+3.0%), the US (+2.8%), and the European Union (+1.7%).

Today, these are the conditions in the last quarter of the 20th Century and into the 21st:

- An abundance of goods/services

- Decrease in demand

- Reduced commercial lending

- Worldwide, cyber and big box store competition

Although the business environment has dramatically changed from the third quarter of the 20th Century, most business managers still view their credit sales and A/R function in the same way as their fathers or grandfathers did in 1955. When asked how credit can best contribute to profitability, most owners, CEOs and managers still say it is all about avoiding bad debt and cash flow. They still focus on the “risk” factor first and foremost and still measure performance by DSO and bad debt.

Being able to control bad debt resulting from credit customers failing to pay and keeping credit customers paying is very important, but that is just a small part of how credit can contribute to profitability.

Risk Management: Tip Of The Credit Iceberg

There are still those who resist the idea that trade credit management is about far more than just “risk management” or mitigation. They cling to DSO and bad debt for KPIs and measurements.

When making changes/improvements, expect resistance. Old orders cling to their ways until there is no choice but to change. But change will always have its way, for efficiency is an inborn human quality — we all have the drive within us to do more/better with the same or less effort.

Bear in mind that 80 to 90 percent or more of all B2B sales involve credit terms, and as commercial lenders have cut back on business lending, the use of Trade Credit has grown. In the U.S., as of Sept. 2009, the spread between business-to-business trade credit and commercial lending had grown by nearly $100 billion since the end of 2008. It will continue to do so.

Consider that accounts receivable (A/R) is one of if not the largest asset of a company selling on credit terms. On average, A/R represents 40 percent of total assets, and as more trade credit is extended this can only increase. A/R is also one of the most liquid assets — being but one step removed from money in the bank.

Remember that while on average 25 percent or more of A/R is past due at any given time (1 day + beyond terms), on average, less than one percent is ever lost to bad debt. There is also the fact that it costs 8 to 14 times as much to sell to a new customer as it does to an existing one, and that the repeat sale is most often the most profitable sale — with each repeat more profitable than the last.

When a business sells products/services on credit — based on payment at a later date — added administrative costs are incurred to gather customer information and evaluate and verify that data.

Other costs include setting terms and conditions of sale, account set-up, billing, posting payments and past due management (not collections). There’s the time value of money cost from carrying A/R and the cost of customers failing to pay. And don’t forget the value of the product itself.

The reasons why any business should create the costs that go with selling on credit are:

1) Customers require time to ensure they received what they ordered before they pay, and they require time to process the billing.

2) Customers need time to add value to the products/services purchased, to make sales to their own downline customers and to receive payment on those sales before they can pay.

3) Credit terms are customary in the seller’s industry and competitors extend credit to customers — part of the “competitive advantage” thing.

The reason any business creates/incurs the costs of selling on credit is to make profitable sales that would otherwise be lost.

Credit is primarily a sales support function. If a company wishes to avoid risk, cash flow delays and bad debt altogether, it should get out of credit and get out of selling. Cash flow is a two-way street — money in and money out. Sales is the source of “money in” and without sales, cash flow stops cold. Yes, risk management is important, but it has to be kept in perspective and not be the tail trying to wag the dog.

In the course of approving credit sales and then working with the issues of past due payments, credit interfaces with just about every facet of a business and has insights that, if understood and used, can help target marketing and sales efforts toward specific customers or markets.

If a supplier fails, its customers can be effected too. Credit can provide an initial (and then on-going) investigation and review of key suppliers. Credit can also support operations by identifying and reporting “areas of opportunity for improvement” throughout the entire chain, thus bringing about new efficiencies that lower everyone’s costs of doing business. It’s that “competitive advantage” thing again; inefficiencies erode competitive advantage by driving up the total cost of doing business — for everyone.

In Closing

Credit exists primarily to capture profitable sales that would otherwise be lost. The credit sales and A/R management function should report directly to the CEO in smaller companies, or to the operations/sales area in larger firms. Accounting/finance has a responsibility to safeguard assets and must have oversight regarding the credit function, as it does with all business functions.

Credit managers can contribute to new efficiencies throughout the entire business chain of suppliers, sellers and customers, if asked.

The credit function can and should support more and larger new and repeat sales, customer service and retention levels, marketing, sales, purchasing and operations efforts, all while maintaining good cash flow and controlling bad debt.

Credit is a lubricant of commerce that allows for the expanded movement of products and services and can contribute to a company’s profitability in many different ways — risk management and good cash flow are the icing on the cake. Trade credit is a 21st Century source of profit . . . waiting to happen. CS

Abe WalkingBear Sanchez is the developer of the copyrighted Profit System of B2B Credit Management: a proven philosophy and set of methodologies that move the credit function from being a cost center to a profit-driven area of business. President of A/R Management Group,Inc. (www.armg-usa.com), Abe WalkingBear Sanchez is also a founding member of the international Profit Centered Credit Group.

www.profitcreditgroup.com.

CONTRACTOR SUPPLY MAGAZINE

The June/July 2026 issue of Contractor Supply magazine is here!

In our cover story, Service Over Scale, Idaho Tool in Nampa, Idaho follows a philosphy of immediacy, expertise, and advocacy through 40 years of change and success.

Also in this issue are Industry Updates.

This digital edition, sponsored by BECK AMERICA Inc., is fully searchable and contains live links to every advertiser and new product listing. Click away!

| Read the Articles Read the Digital Edition |